If you want to lend or borrow on Solana in 2026, two protocols keep coming up: Kamino and marginfi. Both are non-custodial. Both let you deposit tokens for yield, use those tokens as collateral, and borrow against them. Both are Solana-native. But the gap between them, in size, in product strategy, and in fee philosophy, is now huge. This is a head-to-head comparison of Kamino versus marginfi, updated for mid-2026, so you can pick the one that actually fits how you use DeFi.

Quick verdict: which one wins?

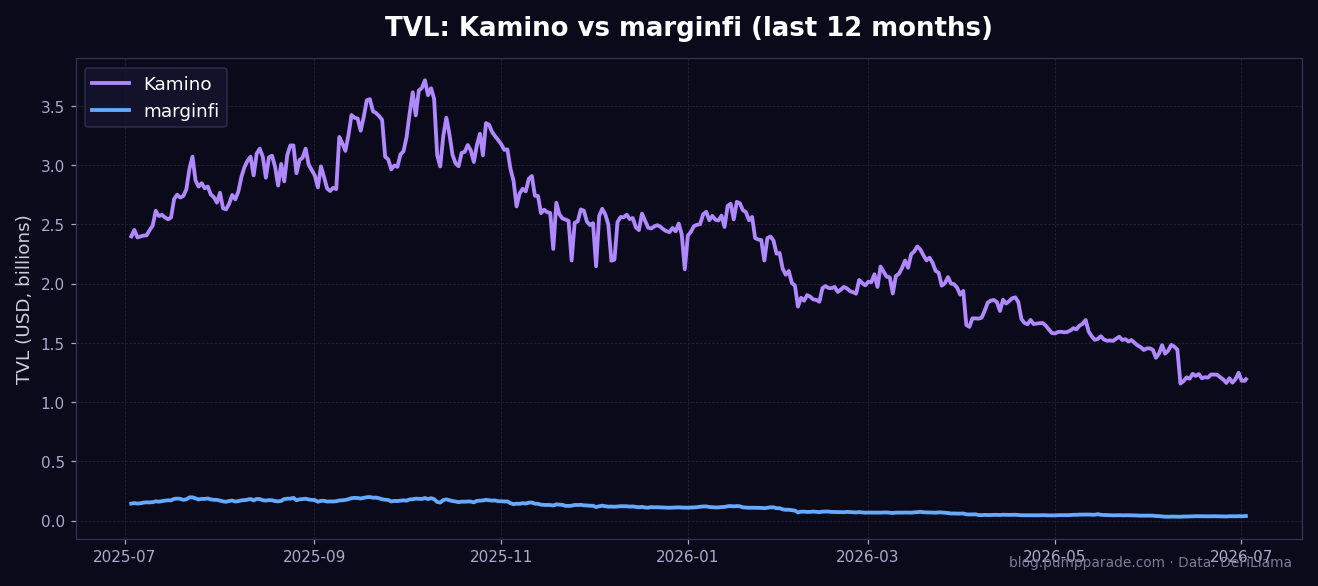

The short answer for most users: Kamino. It has roughly 31x the TVL, a broader product suite that now includes curated lending vaults, leverage, and concentrated liquidity, and deeper reserve depth for large positions in USDC, SOL, and JLP. If you are just here to earn yield on stablecoins or borrow against SOL without thinking too much, Kamino is the safer default in 2026.

marginfi still wins for a specific slice of user: traders who want simple, transparent spread-fee lending markets, native support for staked collateral, and a snappy progressive web app they can use like a mobile app. Loyalists also point to its permissionless, opinion-free bank design as a feature, not a bug. If you value protocol minimalism over TVL, marginfi is not a wrong answer.

The rest of this review breaks down exactly how the two compare on fees, features, security, and real-world UX so you can decide with numbers instead of vibes.

Kamino overview

Kamino started as a concentrated liquidity manager on Orca and Raydium, and has grown into what its team calls a full credit and liquidity suite on Solana. Today the protocol splits into four main products:

- K-Lend, its peer-to-pool borrow and lend primitive, which currently holds around $1.08 billion in TVL according to DeFiLlama.

- Lending Vaults, single-token yield aggregators where a curator allocates deposits across K-Lend reserves so users earn without picking markets themselves.

- Multiply, one-click leveraged positions on assets like JLP, LST pairs, and staked SOL.

- Liquidity, its automated concentrated liquidity strategies on Solana DEXs, which sit around $115 million in TVL.

Aggregated across all products, Kamino carries about $1.19 billion in TVL in mid-2026, which makes it one of the largest DeFi apps on Solana by any measure. Its curator roster now includes credible risk managers such as Gauntlet, Steakhouse Financial, Allez Labs, Rockaway, and Sentora, which is a meaningful signal for anyone worried about parameter risk in a lending market.

If you have already read our earlier Kamino Finance review from April 2026, most of that still applies. The big change since then is the further build-out of Lending Vaults and the growing importance of third-party curators as a first-class part of the product.

marginfi overview

marginfi is a pure play on Solana lending. The core product, mrgnlend, is a straightforward pool-based borrow and lend protocol. Deposit a supported asset into a bank, earn yield, and borrow against your position as long as your account stays healthy. The whole app is designed to feel like a broker terminal for on-chain credit.

On top of mrgnlend, marginfi has shipped a few notable extensions over the last year:

- mrgnloop, an interest-rate arbitrage tool that lets users loop deposits and borrows across banks with one click.

- Staked Collateral, which lets users borrow directly against native SOL stake accounts without unstaking.

- e-mode, higher LTVs when a user borrows correlated assets against similar collateral (for example, borrowing USDC against USDT).

- LST, marginfi’s own liquid staking token, still supported as collateral in the app.

- Progressive Web App, meaning users can install marginfi to their phone home screen and get a near-native mobile experience.

The reality on TVL is less flattering. DeFiLlama shows marginfi holding roughly $38 million in TVL in mid-2026, which is a fraction of where it peaked in earlier cycles. The team has explicitly leaned into being a leaner, more focused protocol with an emphasis on the developer liquidity layer, in-house risk engine, and permissionless bank design.

Head-to-head: features and product depth

Kamino has the wider product surface. In one interface, users can lend, borrow, run leveraged positions, and deposit into curated vaults, all while staying in Solana native assets. That breadth makes Kamino more of a one-stop DeFi hub, which is exactly how the team pitches it in the Kamino docs.

marginfi is deliberately narrower. Its whole thesis is that lending should be modular, transparent, and permissionless. That is why the app is organized around banks (per asset) rather than sprawling multi-asset dashboards, and why so many features (mrgnloop, LST, staked collateral) revolve around better ways to move capital through those banks. The tradeoff is fewer product options for users who want structured yield with less mental overhead.

For sophisticated users, marginfi’s staked collateral and e-mode are genuinely strong. Being able to borrow stablecoins against a native SOL stake account, without giving up the staking yield, is a nice piece of DeFi mechanics. Kamino has its own leveraged staking products through Multiply, but the staked collateral flow on marginfi feels more purpose-built.

Fees compared

The fee models on Kamino and marginfi are meaningfully different, and this is one of the most important sections of any lending review.

marginfi uses a simple interest rate spread fee. According to the official marginfi docs, the protocol takes 12.5% of the interest rate spread on USDC, USDT, and SOL, and 13.5% on every other asset. So if borrowers are paying 10% APY and lenders receive 8%, marginfi captures 12.5% of that 2% spread. On liquidations, borrowers pay a 5% fee that is split between the liquidator and the bank’s insurance fund. There are no fees at deposit.

Kamino is more nuanced because of its Lending Vaults architecture. K-Lend itself uses reserve-specific interest rate curves and no upfront deposit fees. On Lending Vaults, curators can charge a performance fee (a percentage of vault profits), an AUM fee (an annual percentage of vault assets), and a withdrawal penalty that is returned to the vault rather than to the curator. Depositors do not pay a performance fee on a loss, and the withdrawal penalty is a design choice meant to discourage hit-and-run yield farming, per the Kamino Curators & Fees docs.

In practice, if you deposit directly into K-Lend reserves, Kamino can feel cheaper on the surface than marginfi. If you deposit into a curated vault, you are paying for active management, and net APYs can still be very competitive because curators rotate capital into higher-utilization reserves.

Security and audits

Both protocols run in production with meaningful on-chain audit history, but the depth of coverage differs.

Kamino has published audits from firms including OtterSec and Offside Labs, plus a public risk dashboard at risk.kamino.finance. Reserves are governed by Squads multisigs, and market curators can further restrict allocations via a whitelisted reserves feature that hard-codes which markets they are allowed to enter. The Insurance Pool mechanic, in which curators lock their own capital with a cooldown period, is one of the stronger skin-in-the-game features in Solana DeFi.

marginfi has audits on its v2 program and an in-house end-to-end risk engine that continuously monitors bank health, plus a network of in-house and third-party liquidators. The protocol has been running mrgnlend for multiple years without a critical loss-of-funds event, which is meaningful in itself. That said, some coverage is less publicly indexed than Kamino’s, and the protocol’s smaller TVL means less economic security around individual banks in absolute terms.

Neither protocol is risk-free. Oracle failures, extreme market conditions, and smart-contract bugs are always possible. Anyone using either should size positions accordingly and stay away from illiquid, thin banks or reserves.

User experience

Kamino’s app is dense but organized. Everything (Earn, Borrow, Multiply, Swap) lives under one navigation, and vault pages show clear historical APY, allocation breakdowns, and curator identity. On mobile, the responsive web app is usable but not always optimized for one-thumb operation.

marginfi feels lighter. Banks and health factor are the two things you see, and mrgnloop is one of the cleanest looping UIs on Solana. The Progressive Web App means you can install the app to your home screen and get push-style access without a separate mobile build. For users who want a lean, keyboard-friendly on-chain lending experience, this really does matter.

Pros and cons

Kamino: pros

- By far the largest Solana lending protocol by TVL, with roughly $1.19 billion aggregated in mid-2026.

- Wide product suite: K-Lend, Lending Vaults, Multiply, Liquidity, all under one roof.

- Curator-driven vaults offer passive, actively-managed yield without needing to pick markets.

- Serious risk partners like Gauntlet, Steakhouse Financial, and Allez Labs actively curate vaults.

- Insurance Pool and Whitelisted Reserves give depositors on-chain guarantees.

Kamino: cons

- More surface area means more things to understand before your first deposit.

- Curator fees on Lending Vaults can eat into net APY if you do not compare vaults carefully.

- Some Multiply strategies use volatile assets and can liquidate quickly in fast markets.

marginfi: pros

- Very simple, transparent fee model based on interest rate spread.

- Excellent Progressive Web App and mobile UX.

- Native support for staked collateral, so you can borrow without giving up SOL staking yield.

- e-mode allows higher LTVs for correlated asset pairs, which is efficient for stablecoin traders.

- Focused, minimalist product design with fewer moving parts to break.

marginfi: cons

- TVL is now a small fraction of Kamino’s, which means less market depth for large borrows.

- Fewer structured products for passive users who do not want to manage positions.

- Less publicly showcased audit and risk dashboarding compared to Kamino.

When to use Kamino

Use Kamino if you want the deepest liquidity on Solana lending, if you want passive vault-based yield with a real curator behind it, or if you plan to leverage staked SOL, JLP, or LSTs through Multiply. It is also the better choice for larger deposits, because reserve depth matters a lot once you get into six-figure positions.

When to use marginfi

Use marginfi if you value protocol minimalism, if you want a snappy Progressive Web App experience on your phone, or if your workflow revolves around looping stablecoins with e-mode. It is also a good choice for staked SOL holders who want a clean way to borrow against a native stake account.

Rating

Kamino: 4.7 out of 5. The best all-around Solana lending protocol in 2026, held back only by product-surface complexity that can overwhelm new users.

marginfi: 4.0 out of 5. A focused, well-executed lending protocol that has been out-scaled by Kamino but remains one of the cleanest UX experiences in Solana DeFi.

FAQ

Is Kamino safer than marginfi?

Both protocols have audit histories and active liquidator networks. Kamino has larger absolute TVL, more curator-provided risk parameters, and a public risk dashboard, so it has more visible risk infrastructure. marginfi has fewer moving parts, which is a form of safety in itself, but smaller economic security around individual banks.

Which one has better APY?

APYs are market-driven and change constantly. On stablecoins, both protocols typically sit within a few percentage points of each other. Kamino curated vaults can outperform static single-bank positions if a curator is actively rotating capital, but they charge for it.

Can I use both at the same time?

Yes. Many Solana DeFi users split capital between Kamino and marginfi to diversify smart-contract risk and to capture the best rates on specific assets. Since both are non-custodial and connect via wallets like Phantom and Backpack, moving between them is straightforward.

Do Kamino or marginfi have their own tokens?

Kamino has KMNO, its governance and incentive token, which is used across vault incentives and staking. marginfi has run points and incentive programs and has communicated plans around a token in past cycles, but users should always check the official channels for the current state before making assumptions.

Which is better for beginners?

For most new users, Kamino Lending Vaults on USDC or SOL are the easiest starting point. Pick a reputable curator, deposit, and let auto-compounding do the rest. marginfi’s mrgnlend is also beginner-friendly, but the smaller pool sizes and lack of curated vaults mean users need to think more about which single bank to use.

Final take

Kamino has won the Solana lending race in 2026 by a wide margin. It is bigger, deeper, and more composable than any of its peers, including marginfi. But marginfi is still a legitimate second option, especially for users who value focused product design and staked collateral. For a broader DeFi context, we also recommend our Aave 2026 review and Marinade vs Jito comparison as adjacent reading, since staking and lending increasingly compose together on Solana.

Nothing in this article is financial advice. DeFi protocols carry smart-contract, oracle, and market risks. Always do your own research before depositing funds.

{kind=link}