If you have spent any time in DeFi over the past five years, you already know Aave. It is the largest decentralized money market in crypto, the protocol that essentially defined on-chain lending, and the place where billions of dollars in stablecoins and blue-chip collateral sit earning yield right now. But 2026 has been a rough year for DeFi blue chips. With the AAVE token down more than 35% over the last 30 days and lending demand cooling across the market, traders are asking whether Aave is still the safest place to park capital, or whether smaller competitors have finally caught up.

This Aave review covers what the protocol actually offers in 2026, how its fees and yields compare, what makes its risk framework different, and whether depositors and borrowers should still be using it today.

TL;DR Verdict

Rating: 4.4 / 5

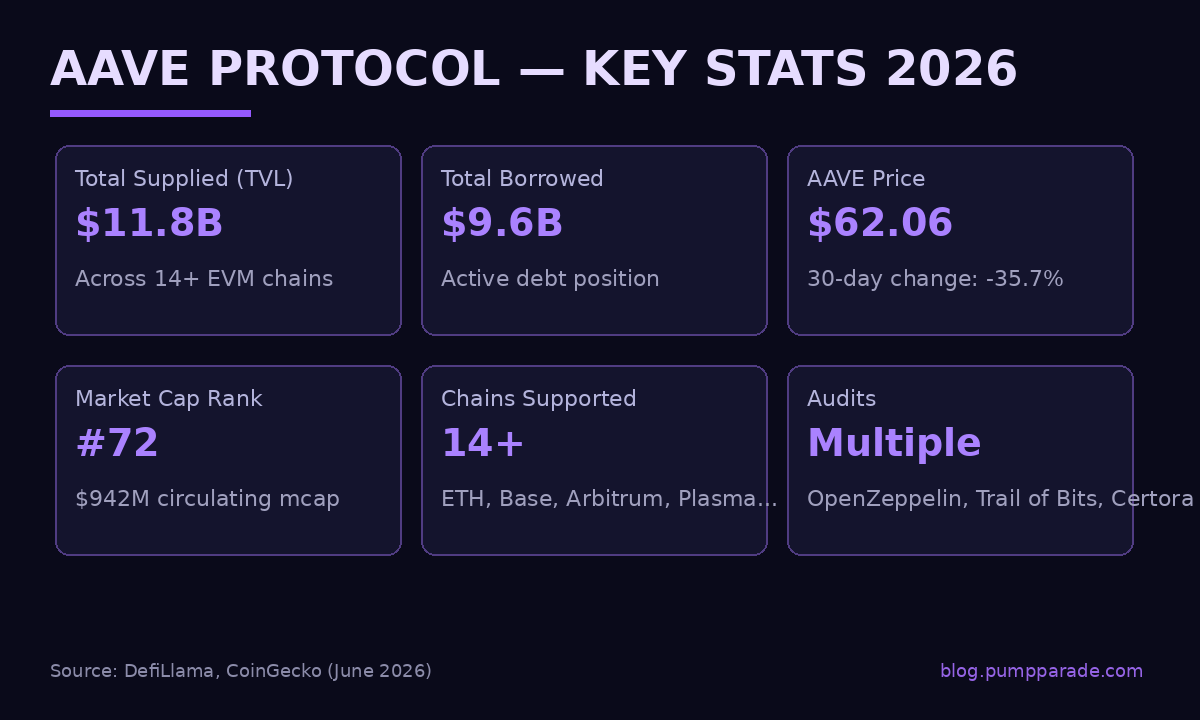

Aave remains the most battle-tested lending protocol in crypto. Roughly $11.8 billion in supplied liquidity sits across 14+ chains, against about $9.6 billion in active borrows, which means the order book is deep enough to absorb almost any retail or institutional position you can throw at it. The v3 architecture, isolation mode, e-mode, and Portal cross-chain plumbing give Aave a risk and capital efficiency stack that no other lender has matched at this scale. The native GHO stablecoin and the Umbrella safety module add upside that previous versions did not have. The downside is that yields on stables have compressed to single digits in the current cycle, the AAVE token has badly underperformed BTC and ETH year to date, and the protocol still carries the complexity of years of upgrades. For depositors who want size and security over the highest possible APY, Aave is still the default. For yield hunters, you can do better on smaller forks if you accept the risk.

What Is Aave?

Aave is a decentralized, non-custodial liquidity protocol. Users supply assets to shared pools and earn variable interest. Other users post collateral and borrow against it, paying interest that flows back to suppliers. There is no order book, no counterparty match, no centralized middle layer. Everything settles on smart contracts and interest accrues per block.

The protocol launched in 2017 as ETHLend, rebranded to Aave (Finnish for “ghost”) in 2018, and shipped its first pool-based lending product in early 2020. The current generation, Aave v3, went live in March 2022 and has been the dominant version ever since. By June 2026 it had been deployed across Ethereum mainnet, Base, Arbitrum, Optimism, Polygon, Avalanche, BNB Chain, Plasma, MegaETH, Scroll, Linea, Sonic, Gnosis, Metis, and several other EVM chains.

You can use the official Aave app directly from a wallet like Phantom, Rabby, or Ledger, or you can interact with the smart contracts through any of dozens of front ends and aggregators. We covered the broader wallet stack in our MetaMask vs Rabby Wallet comparison if you need a refresher on the EVM tooling side.

Aave Key Stats at a Glance

Two notes on these figures. The $11.8B supplied number reflects the sum of TVL across all live v3 deployments. Net deposits available for new borrowers sit at roughly $2.2 billion once you back out current debt. AAVE token data is from the open market and is volatile, treat it as a snapshot, not a fundamental anchor.

Features Deep Dive

Multi-Chain v3 Lending Pools

The core product is the variable rate lending pool. Each market on Aave v3 lists a curated set of assets, sets a loan-to-value (LTV) ratio per asset, and uses a kinked utilization curve to set rates. When pool utilization is low, borrowing is cheap. When it rises above the optimal point (usually 80% to 90%), the borrow rate ramps up sharply, which pulls in suppliers and pushes some borrowers to repay. The mechanism is decade-old at this point and has weathered multiple liquidation cascades without socializing losses to depositors.

Isolation Mode and E-Mode

Two v3-only features deserve attention. Isolation mode lets the DAO list new or riskier assets with a debt ceiling so that any bad debt is contained to that asset alone. E-mode (Efficiency Mode) lets users who only borrow correlated assets, such as stablecoins against stablecoins or ETH against staked ETH, push their LTV up to 93% or higher. For a stablecoin trader who wants to lever a basis trade or a staker who wants to loop into more yield, e-mode is the cheapest place in DeFi to do it.

GHO, the Aave-Native Stablecoin

GHO launched in 2023 and has grown into one of the largest decentralized stablecoins in the market. It is overcollateralized through Aave v3 facilitators, pays a fixed-rate borrow APY set by governance, and burns 100% of interest paid into the Aave DAO treasury. Stakers of AAVE in the safety module get a discount on their GHO borrow rate, which gives the token a real, measurable utility beyond pure governance.

Portal and Cross-Chain Liquidity

Portal is Aave’s native bridge layer, which lets aTokens move across chains by burning on one side and minting on the other. In practice this means a depositor on Ethereum can move liquidity to Base or Arbitrum without exiting their position, and arbitrageurs can keep rates in sync across deployments. It is one of the most underrated features in DeFi.

Umbrella Safety Module

The original safety module let AAVE holders stake their tokens as a backstop. In 2025, the DAO rolled out Umbrella, an upgraded version that lets individual asset suppliers (for example, USDC suppliers on Ethereum) stake their aTokens as their own market-specific insurance, earning extra yield in return. The model spreads risk more efficiently than the old single-asset stkAAVE backstop and is the closest thing DeFi has to a true insurance product at the protocol level.

Flash Loans

Aave invented the flash loan and still has the deepest one. A flash loan lets a developer borrow any amount of any listed asset for the duration of a single transaction, with no collateral, as long as the loan is repaid by the end of that transaction. The fee is 0.05%. Arbitrage bots, liquidators, and refinancers use Aave flash loans constantly, and they generate non-trivial revenue for the DAO without adding meaningful risk.

Fees and Pricing

Aave does not charge a flat trading fee like a DEX. Costs come in three places.

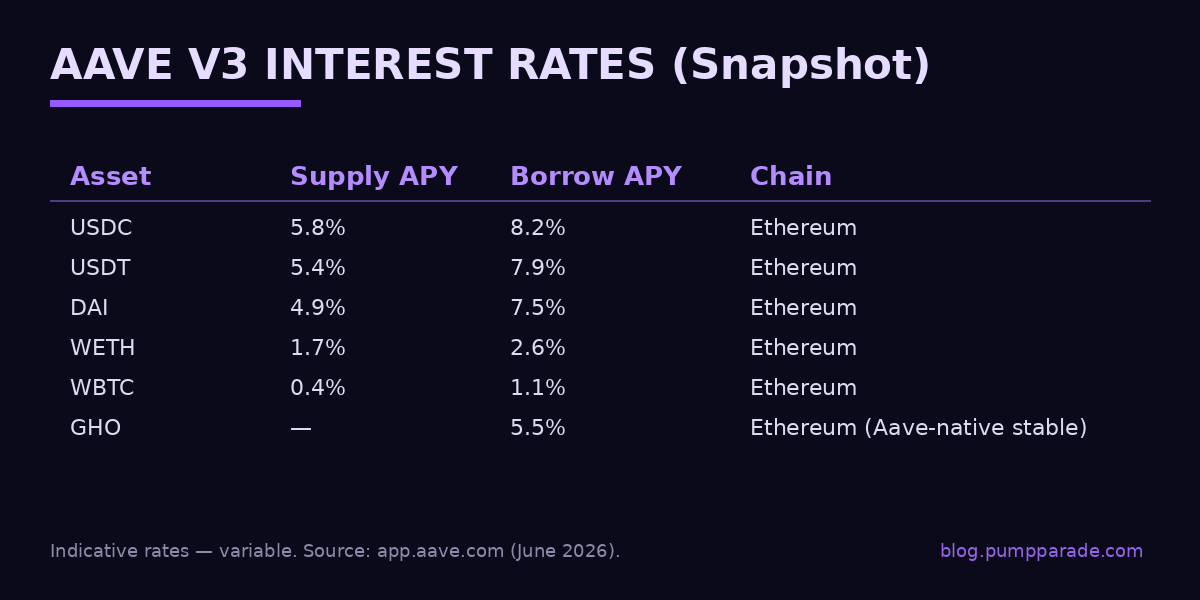

Borrow interest. This is the headline cost. Variable rates are set algorithmically per asset based on pool utilization. Stablecoin borrow APYs typically sit in the 5% to 10% range in 2026, while ETH and BTC borrows run much lower, often under 3%. Stable-rate borrows have been deprecated on most markets in favor of variable-only.

Reserve factor. A portion of the interest paid by borrowers, usually 10% to 25% depending on the asset, is routed to the DAO treasury rather than to suppliers. This is how the protocol funds itself.

Liquidation penalty. If your health factor drops below 1, your position can be liquidated. Liquidators repay part of your debt in exchange for your collateral plus a bonus, usually 5% to 10%. Aave keeps a small slice of that bonus.

Flash loans cost a flat 0.05% of the borrowed amount, paid in the same transaction. There are no deposit, withdrawal, or account fees of any kind. Gas is the user’s problem, which on Ethereum mainnet can be the biggest real-world cost of using the protocol for small positions, and is why most retail users are now defaulting to the Base, Arbitrum, or Polygon deployments.

Security and Trust

This is where Aave actually earns its premium valuation. The protocol has been live for six years across multiple chains and has never had a smart contract exploit that resulted in lender losses. There have been bugs, oracle issues on specific assets, and tail-risk liquidation cascades during market crashes (most notably the November 2022 CRV incident), but no event has impaired the senior deposit claim.

The codebase has been audited by OpenZeppelin, Trail of Bits, Certora, ABDK, Peckshield, and others, with most audit reports linked from the official security page. Certora runs continuous formal verification on the v3 contracts, which catches a class of bugs that traditional audits miss.

Governance is on-chain through the Aave DAO and AAVE token. Most parameter changes (interest rate curves, debt ceilings, listing new assets) flow through a forum proposal and a formal vote. That process is slower than what you get on smaller forks, but it has prevented the kind of unilateral, governance-rug behavior that has killed other lenders.

User Experience

The official Aave app is one of the cleanest UIs in DeFi. The dashboard shows your net worth, total supplied, total borrowed, health factor, and net APY in one screen. You can switch between markets (Ethereum, Base, Arbitrum, etc.) with a single dropdown. Each asset row shows supply APY, borrow APY, utilization, and your individual position. Risk parameters like LTV, liquidation threshold, and reserve factor are exposed in the details panel rather than hidden.

Mobile support is solid through a web wrapper, and the protocol also works fine inside any wallet’s in-app browser. There is no native mobile app, which is a small but persistent friction for users who would rather not connect a wallet from a browser session.

The one piece of UX that still frustrates newcomers is health factor management. Aave does a good job of warning you, but a leveraged loop across e-mode plus the Portal bridge is genuinely complex. New users should start with conservative LTVs and use a position monitor like DeBank or Zapper alongside the app.

Pros and Cons

Pros

- Deepest liquidity in DeFi. $11.8B supplied means almost any size order fills without moving the rate curve materially.

- Battle-tested security. Six years live across multiple chains with no exploit-driven depositor losses.

- v3 features. Isolation mode, e-mode, and Portal are real capital-efficiency advantages that forks have struggled to copy correctly.

- Native stablecoin. GHO gives the DAO recurring revenue and AAVE stakers a real yield kicker.

- Multi-chain reach. 14+ live deployments mean you can stay on whichever chain has the cheapest gas for your size.

- Transparent risk parameters. Every LTV, liquidation threshold, and reserve factor is visible on chain and discussed in public governance.

Cons

- Yields are middle of the pack. Supply APYs on stables sit in the 4% to 6% range. Smaller forks pay more for additional risk.

- AAVE token has lagged. Down 35%+ over the last 30 days and still 90%+ below the 2021 ATH despite strong protocol fundamentals.

- Governance is slow. New asset listings and parameter changes can take weeks.

- Ethereum mainnet gas. Small positions on L1 are economically painful. Use Base or Arbitrum if you have less than $5,000 at stake.

- Complexity ceiling. e-mode, Portal, GHO, Umbrella, and v3 risk parameters together are a lot to learn for a first-time user.

Who Should Use Aave in 2026

Aave is the right protocol for you if any of these describe your use case.

Stablecoin yield with size. If you have six figures or more in USDC, USDT, or DAI, Aave is the safest place in DeFi to earn 4% to 6% with the option to add Umbrella staking on top. Smaller protocols can match or beat that yield but with materially more smart contract and depeg risk.

Leveraged staking and basis trades. e-mode on the ETH/stETH or USDC/USDT pairs offers the cheapest leverage in DeFi for delta-neutral or directional positions in correlated assets.

Borrowing against blue-chip collateral. If you want to hold spot ETH or BTC and borrow stables against them without selling, Aave’s variable borrow APYs on WETH and WBTC are usually under 3%, which is competitive with anywhere else on chain.

GHO minters. Borrowing GHO at the AAVE-staker discount is one of the cheapest ways to mint a decentralized stablecoin in 2026.

If you are primarily chasing the highest possible yield on small stablecoin balances, you may do better on smaller, newer lending protocols, with the obvious caveat that you are taking on more smart-contract risk for the additional basis points. Our earlier Kamino Finance review covers one of the better non-EVM alternatives if you want to compare a Solana-native lender.

Verdict and Rating

Final rating: 4.4 / 5.

Aave in 2026 is what people mean when they talk about DeFi infrastructure. It is the lending venue you reach for when you actually need depth, when you care about your assets being there a year from now, and when you want governance and risk parameters to be visible rather than hidden in a multisig somewhere. The flip side is that it is no longer the highest-yielding option. The market has matured around Aave, which means the easy money has been arbitraged out.

If you treat Aave as a savings layer and a borrowing utility rather than a degen yield play, it is still the best product in its category by a wide margin. Use Base or Arbitrum for small positions, e-mode for correlated leverage, and the Umbrella safety module if you want a bit more yield on your senior deposit. Skip it if you would rather chase 15% to 20% APYs on protocols a tenth of its size.

FAQ

Is Aave safe to use in 2026?

Aave has the strongest security track record in DeFi lending. The v3 contracts have been audited multiple times by OpenZeppelin, Trail of Bits, Certora, and others, and the protocol has never suffered an exploit that impaired depositor balances. That said, no smart contract is risk free. Use sensible LTVs and do not put life-changing money on any single protocol.

What chains does Aave support?

Aave v3 is live on Ethereum mainnet, Base, Arbitrum, Optimism, Polygon, Avalanche, BNB Chain, Plasma, MegaETH, Linea, Scroll, Sonic, Gnosis (xDai), Metis, and several other EVM chains. The largest pool by far is on Ethereum mainnet, but Base and Arbitrum are the cheapest places to use the protocol for retail size.

How does Aave compare to Compound or Morpho?

Aave is significantly larger than Compound and is the protocol Morpho builds on top of in many markets. Compound v3 is simpler but lists fewer assets and fewer chains. Morpho Blue offers more granular vaults but routes a meaningful portion of its activity to Aave underneath. For most users, going directly to Aave is the path of least resistance and lowest abstraction risk.

What is GHO and how is it different from DAI?

GHO is the Aave-native overcollateralized stablecoin. Borrow rates on GHO are set by governance rather than a market curve, which keeps them stable and predictable. All interest paid by GHO borrowers flows directly to the Aave DAO treasury. DAI (now MakerDAO’s Sky USDS) is older, larger, and uses a different governance and revenue model. Both peg to $1.

Do I need to stake AAVE to use the protocol?

No. Staking AAVE in the safety module is purely optional and is mostly relevant if you want the GHO borrow rate discount, governance voting weight, or the extra staking APY. Suppliers and borrowers do not need to hold AAVE at all.

What is the AAVE token’s role?

AAVE is the governance token. Holders vote on protocol parameters, new asset listings, treasury spending, and upgrades. Stakers in the safety module act as a backstop for shortfall events and earn a share of protocol revenue plus emissions. The token is not required for normal protocol use but accrues real cashflow through the safety module and GHO mechanics.

{kind=link}